.svg)

.jpeg)

This is a roadmap for profitable growth if you are a brand with annual shipping costs north of $5M.

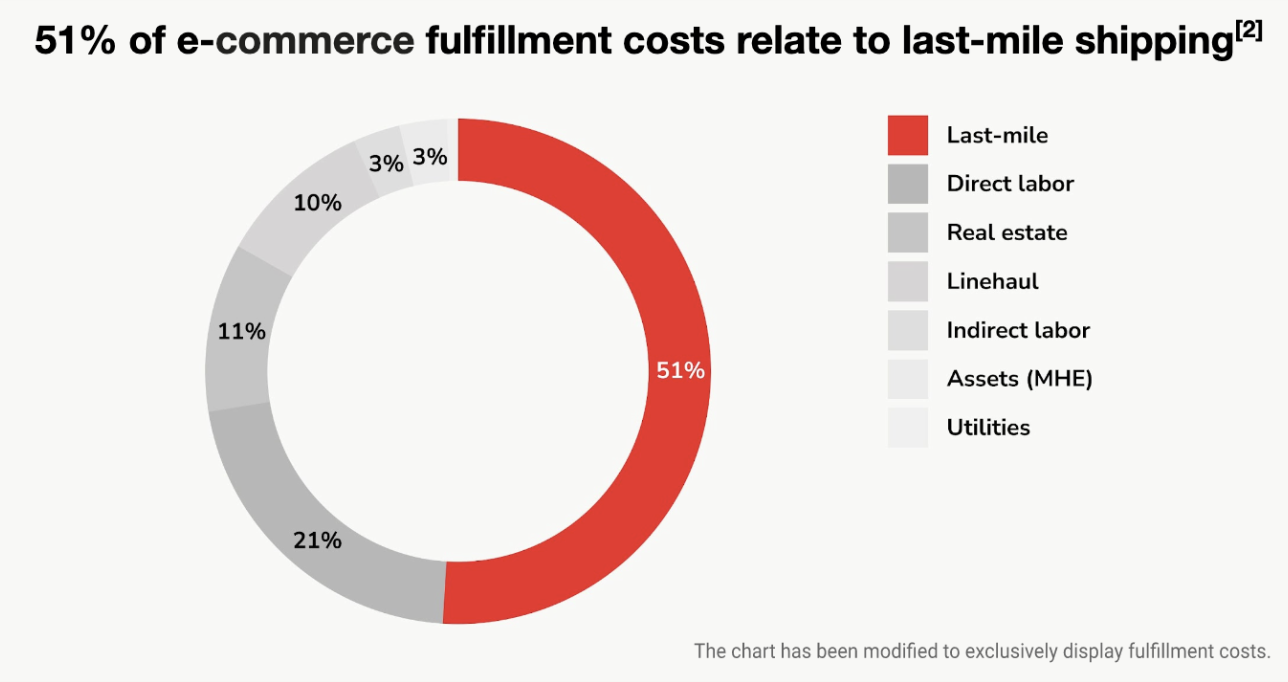

Today’s e-commerce landscape demands a shift from viewing shipping as a cost center to a driver of customer loyalty. The last mile, which accounts for over half of e-commerce fulfillment costs, is a significant brand opportunity. We explore three trends shaping e-commerce shipping and provide action steps for improving shipping performance.

INTRODUCTION

Supply chain leaders need to be more than cost managers; they must take control of growth and innovation at their company.[1] To achieve this, leaders have a golden opportunity to redesign the supply chain. We agree with this strategy, yet competing priorities can lead to a need for clarity on where to drive impact.

Last-mile delivery, the final step in the e-commerce supply chain, presents the most considerable potential for improvement. According to research by McKinsey, logistics costs represent 12% to 20% of e-commerce revenues and will grow to 15% to 25% in the near future. Notably, more than half of e-commerce fulfillment costs relate to last-mile delivery.

Leading brands capitalize on the opportunity by working with innovative shipping solutions like Veho and realize cost savings while elevating the customer experience. A recent analysis by Veho found increasing on-time delivery shipments (OTD) from 92% to 99% and providing real-time text message communication resulted in a 61% reduction in refunds and a 19% increase in repurchases for a top e-commerce brand.

We see three trends shaping the new era of e-commerce shipping and share specific actions supply chain leaders can take to implement winning strategies.

Trends

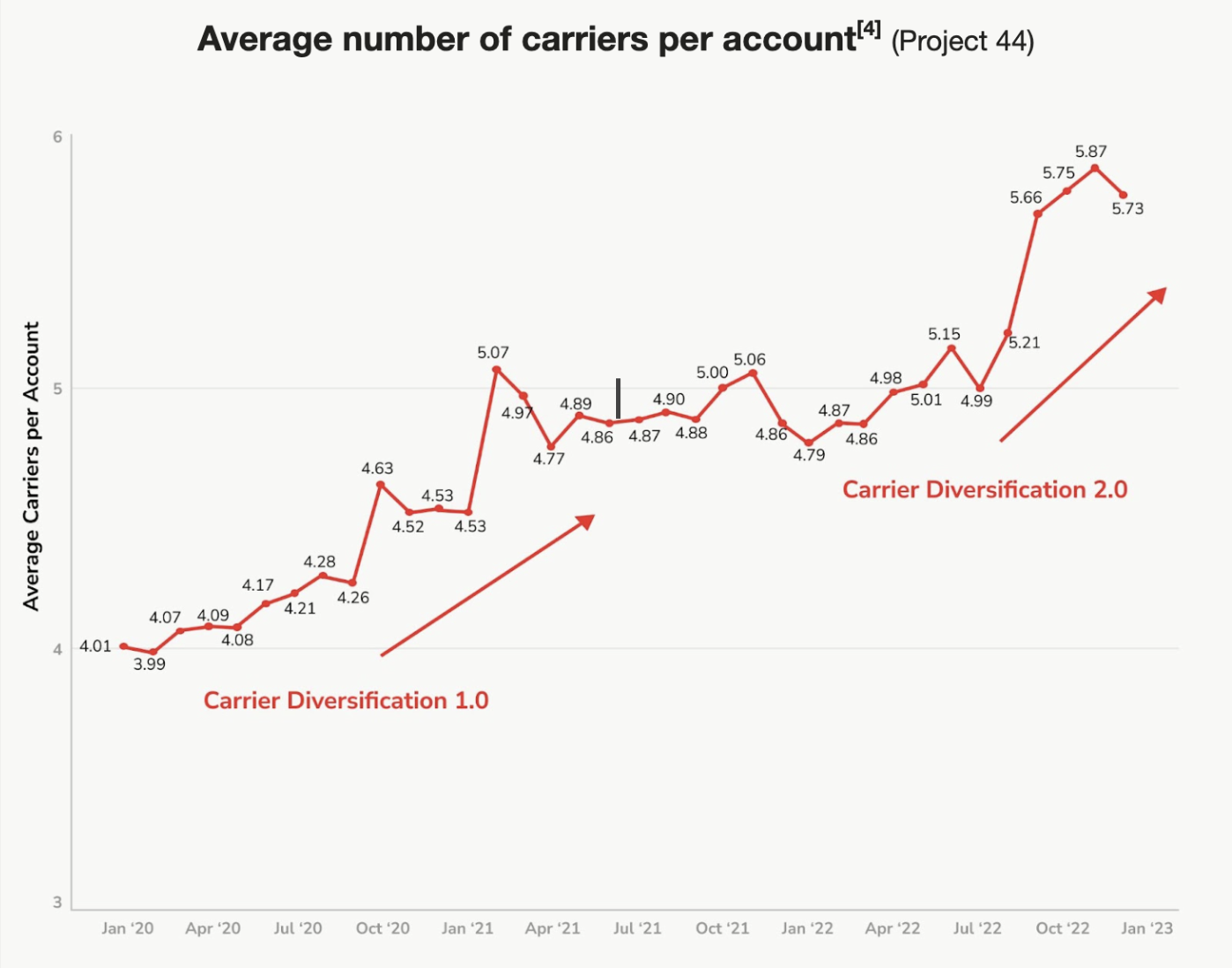

Trend 1: Carrier diversification is accelerating.

The pandemic caused a surge in online shopping, with sales increasing by 43% in the first year.[3] This increase put immense pressure on the shipping infrastructure, causing increased costs, quantity limitations, and deteriorating service quality from national carriers. Leading brands adapted by adding carriers in a wave Veho named Carrier Diversification 1.0.

In today’s economy, carrier diversification continues to grow but with different driving forces. This new Carrier Diversification 2.0 era centers on maximizing the strengths of each carrier within a parcel network. It’s not about piling up the number of carriers—it’s about intelligent allocation. It’s now common for brands to have nearly six carriers in a portfolio.

A recent study from AFS found brands can realize 10-40% savings by working with alternative providers.[5]

SAKARA, a Veho partner, embraces this strategy: “Veho provides a premium delivery experience for our clients while also improving our bottom line. We are actively expanding with Veho in select markets to continue providing best-in-class service while keeping costs at bay.” said Chelsea Clark, Director of Operations & Logistics at SAKARA.[6]

Trend 2: Gig-economy models gain market share.

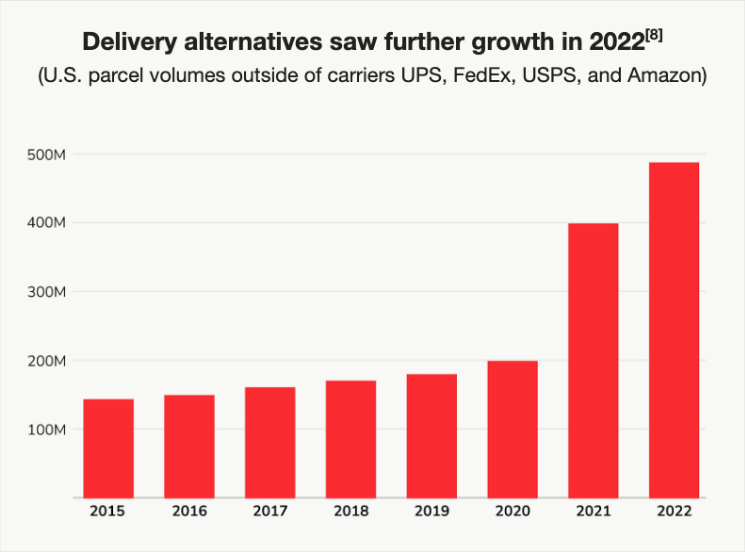

During the pandemic, a staggering $58 billion was invested in supply chain technology, with a sizable share going into last-mile delivery and supporting technologies.[7] After much experimentation with land robots, drones, parcel lockers, and more, the gig-economy model has proven to be the most market-ready technology.

The strength of the gig-economy model lies in its flexibility. It is the only widely deployed system perfectly matching shipping capacity to shipping demand, even during peak season. This innovative approach has gained traction among leading shipping platforms like Veho, as well as major e-commerce brands such as Amazon Flex and Walmart Spark.

.jpeg)

The gig economy model shows no signs of slowing down. According to Pitney Bowes, delivery alternatives have been growing at a pace nearly double their larger, more established counterparts in recent years. Veho's growth outpaces the alternatives and it continues to invest in technology to ensure superior service levels. Bill Seward, the Director of Transportation & Logistics at Saks, believes, “Veho has the future of delivery experience figured out.”

The rise of delivery alternatives benefits e-commerce brands by providing a more comprehensive range of options and fostering innovation. This, in turn, pushes legacy carriers to continuously improve to stay relevant. This year, FedEx and UPS announced billion-dollar investments to keep up with the pace of change. While established carriers slowly modernize, especially regarding last-mile delivery, new-era companies have the advantage of purpose-built infrastructure for e-commerce.

Trend 3: Shipping as a customer loyalty driver.

There’s currently a clear and understandable shift toward cost management by retailers. While some brands are considering eliminating free shipping policies to cut costs, market leaders are enhancing their delivery and return offerings to cement customer loyalty. According to a recent consumer study by Veho, the shipping experience remains a key differentiator in online shopping.

A survey of 1,000 online shoppers found that negative delivery experiences deter 77% of consumers from repurchasing from a brand, and nearly half of all online shoppers associate poor deliveries with the e-commerce brand itself. On the other hand, brands see increased loyalty and sales when providing premium returns and delivery.[9]

This report serves as a wake-up call for brands to rethink shipping, not merely as a cost center but as a strategic lever to drive long-term customer relationships. If you are looking to cut shipping costs and improve customer experience, download the second half of this whitepaper now. It includes a detailed step by step guide, based on our experience working with some of the most advanced shippers in the world.

.png)

.png)